These Apps Can Finally Get You to Save Money

Nothing in the history of money has been more diabolically efficient at getting us to spend than a smartphone. It’s an instant-gratification machine for music, games, takeout and catching a ride, anywhere, all the time.

Now, however, your phone can prevent you from burning a hole in your wallet.

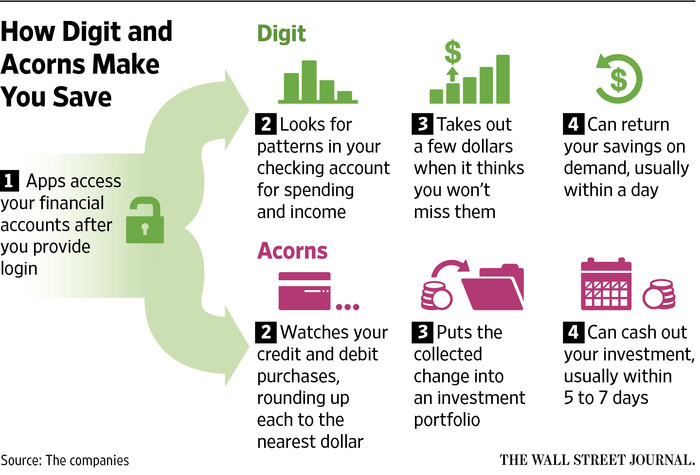

A growing set of apps can help with the self-control that it takes to save money for the future. Apps like Acorns, Digit.co, Level Money and Mint track all the ways you spend to tell you in one glance how to stay on budget. Some even squirrel away extra cash before you blow it.

Apps are key to getting millennials back on financial track. The generation America most likes fretting about—adults under 35—has a savings rate of negative 1.9%, says Moody’s Analytics chief economist Mark Zandi. (The savings rate for everyone 50 and under is also just south of zero.)

But phones are ideal for what behavioral economists, who study the psychology of money, call a nudge: always within reach and can make a game out of guiding us to good choices.

You can read the rest of this article by goinig to the original source: These Apps Can Finally Get You to Save Money – WSJ