A decade ago, the U.S. Congress said companies could tweak retirement plans to get a lot more workers to save. The 2006 Pension Protection Act made clear that employers were allowed to automatically sign up employees for a 401(k), and automatically increase their contribution percentage year after year. Employees could still change their plan or opt out, but most weren’t expected to bother.

At first, companies were enthusiastic. Employers switched to automatic plans in droves. By sparing workers extra paperwork—and making the investment decisions they didn’t feel qualified to make—auto-enrollment could boost 401(k) participation rates as high as 95 percent. Auto-escalation could nudge workers to take full advantage of an employer’s match and save the 10 percent or more of salaries they generally need to retire comfortably.

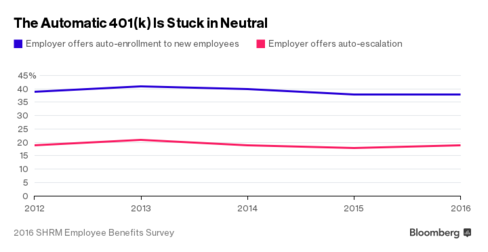

Ten years later that momentum has completely stalled, and it turns out the big reason is cost. According to the latest survey by the Society for Human Resource Management of its HR professional members, fewer than 40 percent of employers offer auto-enrollment for new employees and almost 20 percent offer auto-escalation–numbers that actually fell slightly in the past few years. (This isn’t to be confused with reenrollment, in which employers automatically change the investment mix. Employers can also auto-enroll existing employees, something 21 percent do.)

What’s gone wrong? Retirement experts, including organizations that represent employers and 401(k) plan providers, still enthusiastically endorse automatic 401(k) features. The problem is that companies remain skeptical. The top reason, according to organizations that talk to these holdout employers, is concern about how expensive all this can be.

By getting more workers to increase contributions to their 401(k), you potentially raise the amount you’ll need to pitch in as a matching contribution. If you match the first 3 percent that workers put in, for example, and you get another fifth of your workforce to meet that threshold, then auto-enrollment can look like an expensive decision.

Source: Why Doesn’t Your Company Want You to Put More in Your 401(k)?