The largest tax payers in the US

2013-07-20

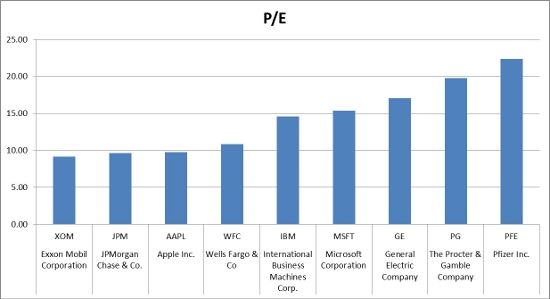

I recently came across this list on Forbes on the largest 25 tax payers. Forbes does a bit of analysis on each of them. It is probably worth your time to jump over, but I thought I would give the highlights here:

|

Rank of tax expense |

Company |

Symbol |

Effective Tax Rate |

| 1 | ExxonMobil | XOM | 39% |

| 2 | Chevron Corporation | CVX | 43% |

| 3 | Apple Inc. | AAPL | 25% |

| 4 | Wells Fargo & Co. | WFC | 31.2% |

| 5 | JP Morgan Chase & Co. | JPM | 26% |

| 6 | Wal-Mart Stores | WMT | 31% |

| 7 | ConocoPhillips | COP | 51.5% |

| 8 | Berkshire Hathaway Inc. | BRK | 28% |

| 9 | IBM | IBM | 24% |

| 10 | Microsoft Corporation | MSFT | 22.8% |

| 11 | Philip Morris International Inc. | PM | 29.5% |

| 12 | Goldman Sachs | GS | 33% |

| 14 | Comcast Corporation | CMCS | 32% |

| 14 | The Procter & Gamble Co. | PG | 23.5% |

| 15 | Johnson & Johnson | JNJ | 23.7% |

| 16 | Intel Corporation | INTC | 23.6% |

| 17 | Occidental Petroleum Corp. | OXY | 42% |

| 18 | UnitedHealth Group | UHG | 35.9% |

| 19 | The Walt Disney Company | DIS | 32.7% |

| 20 | AT&T | T | 27.8% |

| 21 | Oracle | ORCL | 21.4% |

| 22 | The Coca-Cola Company | KO | 23.1% |

| 23 | The Home Depot Inc. | HD | 37.2% |

| 24 | McDonald’s | MCD | 32.4% |

| 25 | GOOG | 19.4% |