How big is the iPhone? Bigger than most companies.

This is not an Apple [stckqut]AAPL[/stckqut] fanatics site but the importance of the iPhone to the technology world and the market in general is rare. There are few products, that if turned into standalone companies, would be as significant as the iPhone.

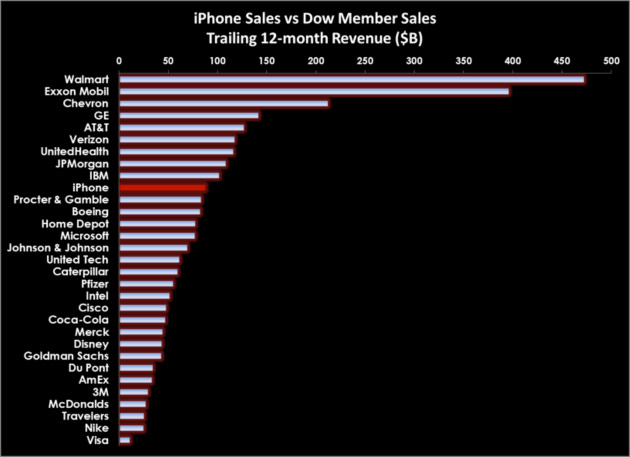

As an example, if the iPhone was a standalone company it would have revenue of $88.4B. This means that it would rank 28th on the Fortune 500 and would be between Archer Daniels Midland [stckqut]ADM[/stckqut] and Procter & Gamble [stckqut]PG[/stckqut]. In fact, if Apple spun off the iPhone, Apple would drop to 30 or 31 on the list from its current 6th place and iPhone Inc. would be larger.

BusinessWeek points out that the new company, iPhone Inc., would be the 9th largest company on the Dow Jones Industrial Average.

There is nothing that will destroy your ability to save money for the future and invest in your own welfare like living beyond your means. I am often told by my readers (by

There is nothing that will destroy your ability to save money for the future and invest in your own welfare like living beyond your means. I am often told by my readers (by