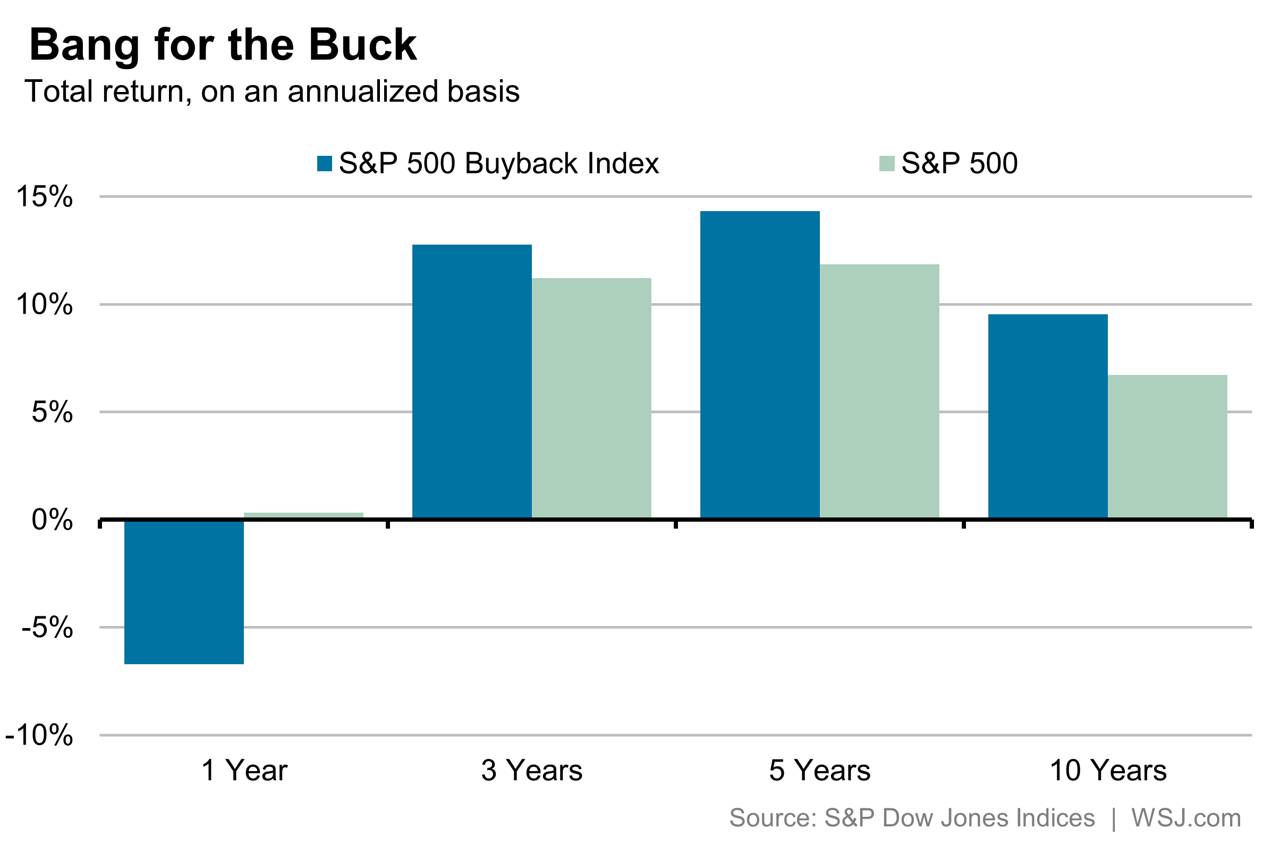

The corporate buyback binge continues at full tilt. But, perhaps with good reason, investors may be losing faith in its ability to propel share prices.

U.S. companies authorized $158 billion of new stock buyback programs in January and February, according to Birinyi Associates Inc. While there is no guarantee the rest of 2016 will maintain such a pace, it marked the best start to a year since the research firm started tracking this data in 1984.

I am not a big lover of companies that buyback their stock from the market. In general, I prefer a company that has so many great ideas for new products and new services that they want to invest in their future potential.

Companies have limited cash. The management of the company along with the Board of Directors has to decide the best use for that cash. Do they save it for a rainy day, do they invest in new products, or do they return that money to their shareholders. It should all be summed up with a simply question: What will make the company more valuable?

I feel that a signal of a company that has stagnated is a company that cannot figure out how to grow the company with new products and services. While the short-term goal of moving the stock up in value with a buyback is nice, it simply means the company is at risk of being a great provider in the next couple of years.

There are situations where a buyback is worthwhile. Most notably, this occurs in companies that have large R&D budgets. Especially, if those budgets are larger than their direct competitors. In that case, the company is investing in its future and increasing the short-term stock price.

So, one explanation for the sputtering Buyback Index is that investors smell trouble. Another explanation is more benign: That there are more investors like me that are optimistic about the economy and are rewarding companies that plow money into productive assets.