The environment still looks more friendly for stocks than bonds. Global growth is broad and momentum appears good. Earnings have recovered and are forecast to rise further around the world in 2018.

And the environment still looks more friendly for stocks than bonds. Global growth is broad and momentum appears good. Earnings have recovered and are forecast to rise further around the world in 2018. U.S. stocks may look stretched based on rising earnings multiples, a red flag in investors’ minds, but in Europe, for instance, it is earnings that are doing the heavy lifting. Many emerging-market economies are much earlier in the cycle too. Investors might need to look further afield for returns.

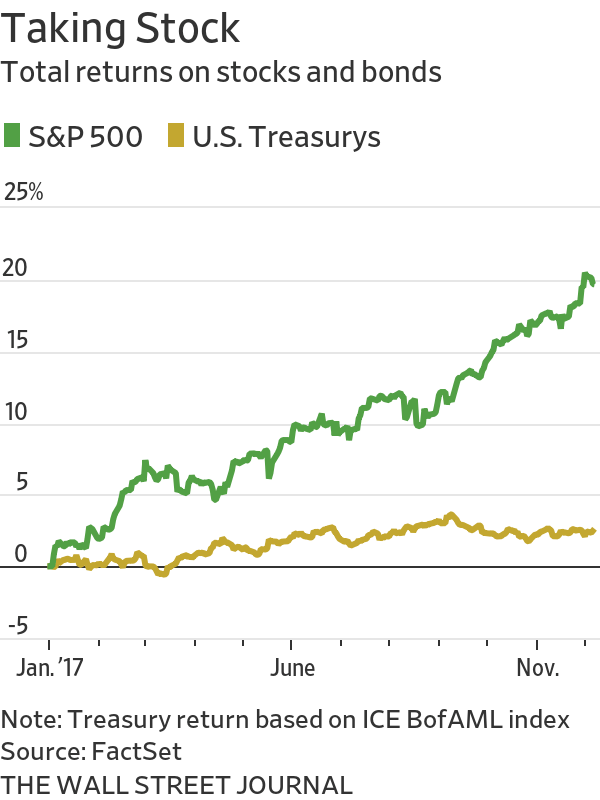

Importantly, equities remain a place where investors still get paid for taking risk. The MSCI World equity risk premium has fallen, but still stands at 3.8%, above its postcrisis lows and its 2007 level of 3.3%, according to Citigroup.

By contrast, low bond yields and tight corporate-credit spreads offer little room for error. That means a scenario that is worrying bond investors—a more challenging 2018 in which inflation picks up, eroding already-skinny returns and potentially spurring further central-bank tightening—may pose less of a threat to equities. The risk premium offers some room to absorb higher yields.